Canadian Bonds: What Are They Telling Us About the Future?

An Insight into Government Bond Rates

Despite multiple interest rate cuts, Canada has yet to see a significant resurgence in housing demand.

A major hurdle to increased demand is that bank prime rates haven’t fallen as quickly as the overnight rate, keeping mortgages relatively expensive. Why is this happening?

One key factor is bond rates, which banks consider when setting their prime rates.

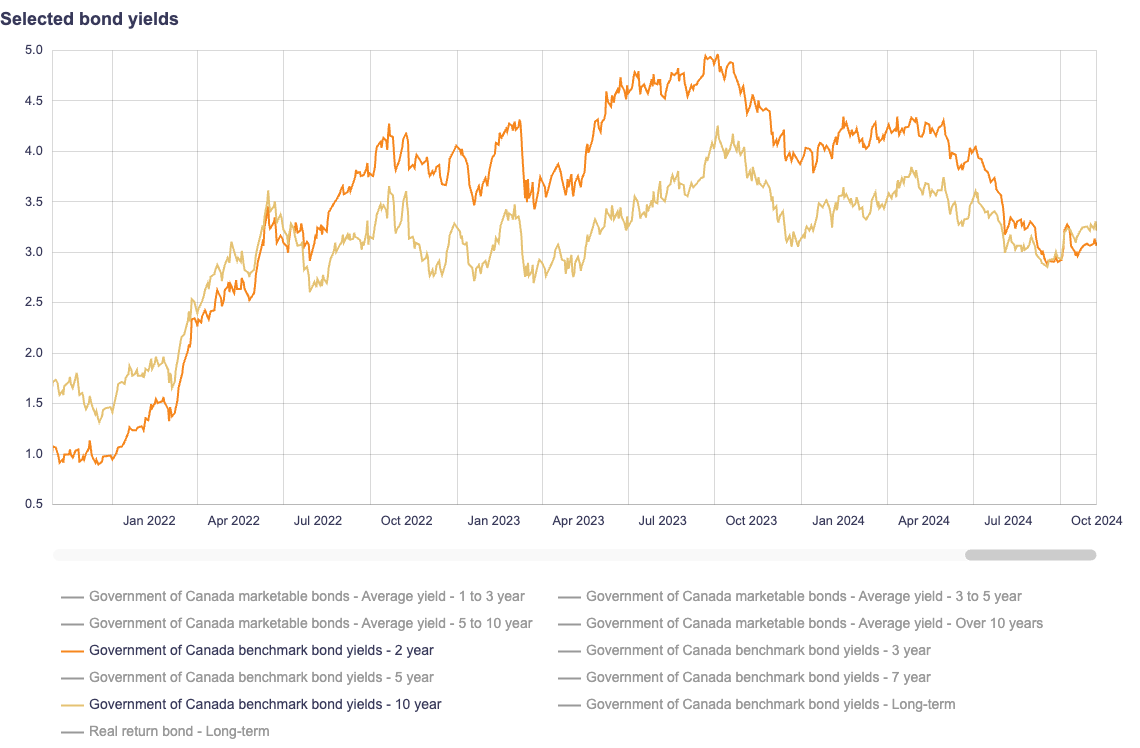

Lets take a look at the Canadian Bonds comparing the 2 year and 10 year yields from the BOC website.

In the chart above, we see rates over the period from January 2022 to the present. The 2-year rate (short-term) is shown in orange, and the 10-year rate (long-term) is in yellow.

Between April and July 2022, the two rates crossed, with the long-term rate falling below the short-term rate. This period coincided with the central bank's initiation of overnight rate hikes. The spread between these rates continued to widen until the short-term rate peaked around September 2023, before beginning to tighten until July 2024.

It wasn't until October 2024 that short-term rates finally dropped below long-term rates again.

When long-term rates fall below short-term rates, it creates what’s known as a yield curve inversion, typically viewed as a warning sign of future economic challenges, as it signals the market’s expectation of rate cuts ahead due to potential economic downturns.

A reversion of the yield curve, where short-term rates fall below long-term rates again, suggests we are nearing the bottom of an interest rate cycle, often followed by inflation. Inflation generally leads to a period of heightened economic activity, increasing demand across assets and raising prices.

Let's examine previous inversions and reversions over the past 20+ years to see how these patterns align historically.

Here are some key milestones for the points on the chart above:

2001: Following the 9/11 terrorist attacks, we saw short-term rates drop amid heightened uncertainty in the global market.

2006: The rate spread began to narrow, fluctuating closely and crossing several times until the 2007-2008 recession, when short-term rates dropped sharply.

2008 to 2018-2019: This period saw a wide spread between the rates, marking one of the longest-running economic booms in history.

2018: The spread began to tighten again, until COVID-19 hit in 2019.

2020: Rates were drastically cut once more, with short-term rates dropping below long-term rates. This period was notable for the real estate boom that followed.

2022: The central bank started raising overnight rates again, tightening the spread to an unusually large reversed spread, though without a classic inversion. (This unique situation merits a deeper look in a future analysis.)

Now (2024): The spread has recently tightened again, with short-term rates now lower than long-term rates for only about a month. While it’s too early to draw conclusions, this could signal an impending decrease in prime and mortgage rates, potentially followed by an economic boom if conditions align.

The spread has finally tightened again, bringing us back to that pivotal moment where short-term rates have dropped below long-term rates! This shift may have only been in place for about a month, but it’s an exciting signal. If this trend continues, we could be on the brink of lower prime and mortgage rates—potentially setting the stage for a strong economic upswing. This could be the momentum we’ve been waiting for!